Payments vs Transfers

Every so often, somebody will tell me how crypto will render Visa and Mastercard obsolete. Crypto could do that one day but what we have today is not enough. Other people tell me that crypto is terrible, Visa is also terrible, and that payment fees should be absolutely zero. In both cases, when they run me through the logic, I often realize that they don't understand the difference between payments and transfers:

- A transfer is the simplest operation: you move money from account A to account B. They are usually irreversible1 and in many cases, the same entity often controls both accounts. For example, you send money from your bank to your broker.

- A payment is made in exchange for goods and services and it has an implicit contract associated. The rules of this implicit contract are codified in the payment network rules.

Sending USDC over the Ethereum network solves the transfer use-case but not the payment use-case. Would you send an irreversible USDC transfer to a merchant that you've never heard of before? Most people wouldn't.

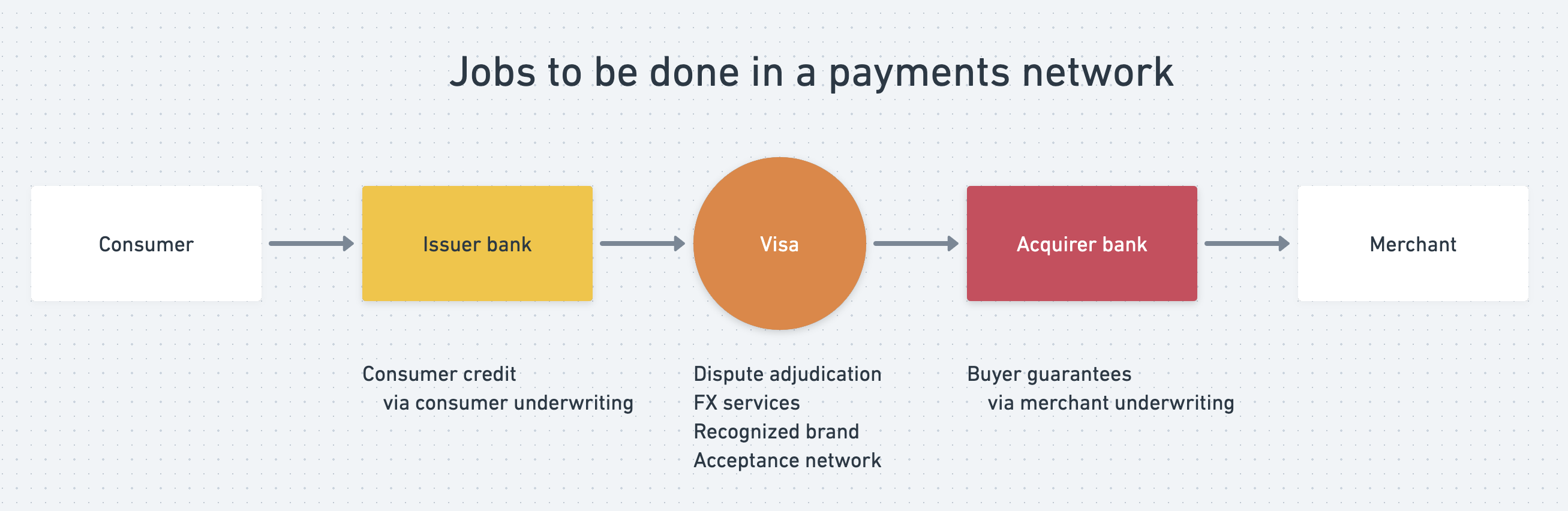

The value of a payment network

We could absolutely build a crypto payment network (and that would be great) but it is important to recognize what are the many functions of existing payment networks before calling them obsolete. For payments to work well, you need:

- Buyer guarantees

- Credit for the buyers and seller's guarantees

- Dispute adjudication

- Foreign exchange services

- A recognized brand and an “acceptance network”

- Compliance

1. Buyer guarantees

If sellers don't deliver the goods, buyers want to know they’ll get their money back. This requires somebody to onboard and control the sellers and take the risk if one of the sellers runs away with the money before delivering the goods.

In the Visa network, this has been done historically by "acquirer banks" that have relationships with merchants. Wells Fargo, Chase, and Bank of America all have an acquiring business. In the last 15 years, acquirer banks have passed on the burden of onboarding and underwriting risk to payment processors like Stripe and Square. Commerce is growing too quickly for banks to underwrite everybody that wants to set an online store.

When underwriting merchants, the key variables are:

- Certain industries like cruise ships and events have a long return window: they charge you today but deliver their services in 6 months or more. The payment processor accrues risk proportional to that return window. If a grocer goes out of business, there is a week or two of payments to refund. But if a cruise company goes out of business, there are +6 months worth of payments to refund.

- Those industries also have highly correlated refunds: one canceled cruise ship is a lot of refunds. Cruise companies are likely to go bankrupt if their cruises have to be canceled because they simply can’t pay all those refunds at the same time.

- Overall fraud rate of the industry: the gift card industry is prone to scams, so acquirers have learned that merchants routinely run away with buyer’s money at a higher-than-usual rate.

Cash doesn't have buyer guarantees and as such, people are wary of using it for large purchases to be delivered later (but are fine with using it to buy chocolate in a kiosk).

Cost: Buyer guarantees have a cost directly proportional to the total payment.

2. Credit for the buyers

Consumers spend a lot more if you give them credit. Merchants (with high margins) are usually happy covering many of the associated fees because they make it up in increased volume. In the Visa network, card issuers like Chase and Capital One provide that consumer credit when they issue you a credit card and a credit line.

Debit cards are also issued by these issuer banks and part of the payment network but they have no credit associated. And as you'd expect, the average order value of debit cards is often much lower than credit cards, even for the same merchant2. If the consumer defaults on their credit, it is the issuer's problem. Merchants don't need to be underwriting each customer individually.

Buyer’s credit was not invented by card networks. Stores used to extend credit to its buyers and keep a tally of how much each one owed (before computers!). One of the main innovations of the card networks was managing this credit for smaller merchants3 and one of the reasons that merchants were happy to accept them. From Chapter 1 of Electronic Value Exchange4:

[A merchant] had three girls working on Burroughs bookkeeping machines, each handling 1,000 to 1,500 accounts. I looked at the size of the accounts: $4.58. $12.82. And he was sending out monthly bills on these accounts. Then the customers paid him maybe three or four months later. […] His accounts receivables were dragging him under.

Most consumer credit in the US is revolving credit: you draw from it as you buy things, and you pay your outstanding balance wherever you can. But credit can take many forms:

- In LATAM installments are more popular: you buy an item today and pay over 12 installments, one a month (“coutas” in Argentina, “parcelas” in Brazil, “meses sin intereses” in Mexico).

- Buy Now Pay Later (BNPLs) are the latest form of consumer credit: you pay in 4 installments, every two weeks to match salary payments. This is increasingly popular where revolving credit is popular but not really interesting wherever installments are already common.

Cost: Providing credit has a cost proportional to the amount of the purchase.

3. Dispute adjudication

When buyers and sellers disagree, the network needs to adjudicate the dispute. This is expensive because it requires human attention and nobody wants to do it. Neither the seller nor the buyer (or any agents that represent them) can credibly do this work, so you need a third neutral party. In the case of Visa, it is supposed to be the network but in practice the issuers do some of this work, which is why merchants largely lose disputes.

This is not always necessary. Buyers trust aggregators like Amazon to return their money if there is a problem. But without buyer guarantees and a dispute system, smaller merchants have a harder time getting off the ground.

Cost: Adjudicating disputes has a fixed cost per dispute, but a high one.

4. Foreign exchange services

Let’s say the buyer wants to pay with 100 USD and the merchant wants to receive 100 EUR (on the purchase day the FX rate was 1:1). Somebody needs to:

- Provide the seller’s currency (EUR) and take the buyers currency (USD)

- Nobody naturally wants to be holding all sorts of currencies. FX rates fluctuate everyday and you need to be very careful if you are exposed to those fluctuations.

- Hold the FX risk during the return window

- Two months after the purchase, the buyer asks for a refund. The FX rate is now 1:1.2. The merchant wants to return 100 EUR but at current rates, that is no longer enough to cover the 100 USD the buyer wants to receive. Somebody needs to produce the missing USD. Who is holding that risk?

Cost: Both of these services have a risk proportional to the total amount of the payment.

5. A recognized brand and an “acceptance network”

Consumers only know to pay with a “payment method” if it is advertised to them often (i.e. a brand) and there are a lot of merchants that accept it (an “acceptance network”). The network effects in payments are very strong. You know how all shops have Visa and Mastercard signs5 stuck to their windows? It takes a lot of work to make that happen in most of the world. A global payment network doesn’t just manifest!

Cost: The cost of maintaining this network and brand is not linearly related to the network's processing volume but definitely proportional.

6. Compliance

You may not think as compliance as "a job to be done" but as soon as regulators start chasing you, you will! The regulators want to prevent certain goods and services to be exchanged for money (drugs, sex, etc.) and they pressure anything that functions as a payment network to do their bidding.

This is far from perfect but it allows large companies and the government (large sectors of the economy) to use the card networks.

While keeping compliant is a value-proposition to most actors, it less important for decentralized systems like crypto6.

Transfers have fixed costs, payments have variable costs

Transfer systems are much easier to set up because they don't provide all these services. Importantly, they can have “fixed” costs where the cost of a transaction is not proportional to the amount of the transfer. The transfer system is not exposed to any variable costs.

But as you saw, 4/5 of the payment services have variable costs and as such, need to have a variable rate to operate.

Problems with the card network

If you want to build a new payment network, here are some places where the current dominant networks are failing for the US market7:

- Relatively low conversion rates

- High fraud rates

- Card networks pass the fraud burden to merchants

- Debit card consumers subsidize credit card consumers

- Creeping costs

- Slow settlement time

- Not all consumers can participate

- Many legitimate industries are deemed risky or illegal

1. Relatively low conversion rates

Online, cards are actually a pretty bad payment method. Entering the 16 digit number is a pain, which is why you are so grateful whenever Apple Pay, Shopify's Shop Pay, or Stripe’s Link are on the page ready to autocomplete all the information you need.

I worked on Link and I’ve seen first hand the conversion lift that it can generate. It is crazy that most merchants still ask you to enter the 16 digits!

2. High fraud rates

Every large merchants needs to have an in-house team dedicated to preventing fraud. This is a drag on the online economy and completely unnecessary.

Fraud should largely be solved with better technology. Apple Pay8 works on top of the card networks and has at least one order of magnitude less fraud:

- When you onboard a card to the Apple Pay wallet, the issuer authenticates and Apple Pay authenticates you with Face ID or Touch ID.

- Each time you set up a card with a merchant, Apple Pay generates a new set of 16 numbers and encrypts them in your device before passing them around.

- They only do this if they were able to authenticate you with Face ID or Touch ID, like you did in the setup.

- When the issuer gets one of these encrypted numbers, they can trust that they came from the Apple Pay wallet and, if they trust Apple's authentication, that it was the real consumer.

Visa still hasn’t provided for all their transactions but a new payment network would certainly provide similar guarantees.

3. Card networks pass the fraud burden to merchants

Online merchants are on the hook for any fraudulent transaction which is maddening to first-time merchants9. This effectively requires merchants to underwrite each customer individually the first time they come to the store. In these cases, merchants are getting a lousy deal; they are covering the payment network fees without getting the basic value that they are supposed to provide.

This is especially bad for low margin business: imagine you have a 5% margin and you keep $5 every $100 of sales. Each fraudulent transaction costs you ~$95 but each good one gets you back $5. So, to make up for each fraudulent transaction you need to sell an additional 19. Low-margin merchant have to be much more careful about fraud10.

4. Debit card consumers subsidize credit card consumers

Card issuers like Chase and Capital One compete to get the richest consumers. To do that, they lobby Visa to get higher fees from their premium cards and then they pass part of those fees back to the consumer, bribing them to use their card. This is what a points or a cashback program is. The fees for some of these cards end up amounting to 2% or more.

But who is paying for those points and rewards? Let’s think step by step:

Before cards, supply and demand force the merchant to charge an average of $100:

| Consumer that would use debit | Consumer that would use credit | |

|---|---|---|

| Consumer pays | $100 | $100 |

| Merchant gets | $100 | $100 |

Once they introduce cards, merchants initially keep the same price and they discover a 1% fee for debit and 2% for credit11:

| Debit consumer | Credit consumer | |

|---|---|---|

| Consumer pays | $100 | $100 - $1 rewards = $99 |

| Merchant gets | $99 | $98 |

Assuming a 50/50 credit-debit split, the average amount the merchant is receiving is $98.5. This is significant. The merchant would like to charge $102 to the credit card and $101 to the debit card but Visa rules prohibit this.

To make up for those fees, they increase the price to $101.5 or so for all consumers. They can do this because every merchant also has to do this and the fee won't be competed away.

After merchants increase to $101.5 to get back to their original target margin:

| Debit consumer | Credit consumer | |

|---|---|---|

| Consumer pays | $101.5 | $101.5 - $1 rewards = $100.5 |

| Merchant gets | $100.5 | $99.5 |

You can now see that:

- The merchant is making more margin from debit consumers

- But overall, the merchant is actually getting what they were getting before.

- The debit consumer is effectively paying an extra 1.5% than what they were going to pay

- The credit consumer is paying what they were going to pay before.

At the end of the day, it is cash and debit card users who are paying for your Chase Sapphire points.

In this process, I've omitted cash users but you can see that they are equivalent to debit card users in that they pay $100 and get no benefits12. Who Gains and Who Loses from Credit Card Payments? Theory and Calibrations has a more detailed model of this process and estimates the overall effect on households:

On average, each cash-using household pays $149 to card-using households and each card-using household receives $1,133 from cash users every year.

5. Creeping costs: merchants don’t have enough choice

As noted above, merchants can’t charge different prices for consumers that are going to get rewards. If the Visa network adds more expensive “payment methods” that are unappealing to low-margin merchants, those merchants can’t really choose if they want to accept them. Coupled with the fraud costs, this makes low-margin merchants unhappy with Visa.

You can see this dynamic playing out differently with Buy Now Pay Later. BNPLs took off during the last couple of crazy years. It sounds like a great idea for high margin merchants which are happy subsidizing credit for certain purchases. But low-margin merchants don’t want to pay 5-6% for BNPLs. Given that BNPLs are outside of the Visa network, that is fine: each merchant can choose what they accept and that is roughly what you see in the market.

6. Settlement time

In the US, merchants typically get paid 2 days after the purchase was completed. While this doesn't sound terrible, it could be better. Many merchants (like Instacart and Lyft), want to pay their vendors (shoppers and drivers) right away.

Visa is a net settlement system: acquirer banks (and merchants) are paid in batches of payments, net of fees, disputes, and refunds. In a net settlement system you'll always have to wait to get a payment until the batch is ready. But how much you wait after the batch depends on how slow the underlying system is. In the US, using ACH credit transfers that is 2 days:

- One day for the issuer bank to net with the acquirer bank

- A second day for the acquirer bank to send the money to the merchant's corporate bank.

If there is anything that new systems like RTP will do well, is this: speed up B2B transactions, including card network settlements and get merchants their money faster.

This timing is region-specific. In Brazil, the network pays you 30 days after the purchase, which creates a credit card for "anticipations" that nets as a an additional interest fee of 0.3% to get your money quickly.

7. Not all consumers can participate

In the US, it is only issuers banks who can issue cards. These banks have high fixed costs in the form of branches and can only profitably serve customers that are relatively rich. Those who are not rich enough to be served by one of these banks (e.g. Wells Fargo).

This is rarely implemented with a large sign that says "Poor People not Allowed". Instead, banks put fees for holding a minimum balance ("We debit you $10 if you have less than $100 in your account"), which poor people can't really afford.

This has changed in the last 10 years with fintech's and neobanks like Cash App and Ally Bank which provide bank services (and even cards!) but don't have branches and none of the fixed costs so they can serve poorer customers and still make money. This is also a problem (and a larger one) in the rest of the world (LATAM) and is being largely solved by neobanks like Nubank.

8. Many legitimate industries are deemed risky or illegal

Risk

The card networks have no problems with some industries like dropshipping or cruises. But they go out of business suddenly causing losses for the payment processors. For these industries, it would be better if the payment network could accommodate a modified contract with the consumer:

You are paying a merchant that is in a risky industry. If they go out of business before they deliver the goods, you may not get a full refund.

I am not sure if consumers would actually like this but it would allow for certain activity to happen that otherwise doesn't.

Illegal but legitimate industries

Consumers and regulators don't always agree on what products and services should be legal or illegal to sell. My sense is that right now in the US, regulators are more restrictive than what the median consumer would like them to be.

Certain products like weed are widely demanded by people but still rejected by default by the card networks. This is clearly the place where crypto can provide the most value. Crypto doesn't need to be regulated to exist.

Conclusion

Crypto could build a competitive payment network13 but before doing that, the industry needs to understand that these services matter. In the card networks, these services are provided by certain institutions (issuer banks, acquiring banks) following certain rules and incentives (interchange, underwriting risk). The Ethereum ecosystem in particular is interested in incentive and institution design, and as such is best position to implement a competitive payment network (in my opinion). But there is a lot of work to do to get there.

These services don’t matter in all contexts and they don’t matter for all merchants or consumers. But in markets with established payment networks like the US or Europe, transfers won’t cut it.

Thanks to Jack Dent, Luke Constable, Matt Brown, Lachy Groom, and Vitalik Buterin for reading drafts and providing valuable feedback.

Footnotes

- Not necessarily literally irreversible but rather, usually expected to be irreversible, with the system designed for that. How this works in practice is well-covered by Bits about Money↩

- This might be a correlation though: the people with the capacity to get credit are the ones that spend more. My hypothesis is that this effect greatly depends on the demographic: for some demographic having access to credit does cause more spending, for others it doesn't matter, and the effect we see is a combination of both.↩

- Larger merchants like Sears had established card programs of their own and the capacity to run them and internalize the benefits.↩

- I can’t recommend Electronic Value Exchange enough. It is the best way to understand the payments industry and a great socio-technical account of how a complex piece of infrastructure is conceived, built, and evolved.↩

- These are called "acceptance marks" and payment companies think a lot about them, including contract clauses about how and where they must be displayed.↩

- In fact, the place where crypto provides great value is in not needing to be compliant.↩

- I know much less about other markets but my understanding is that some of these problems are the same or worse and others are non-existent. For example, the EU capped fees so rewards are not a problem. In LATAM, conversion rates are much lower and fraud is much higher. Depending on where you go, there are other new and local problems, like Brazil's long settlement time.↩

- For more on Apple Pay, see this guide↩

- This post from Candy Japan captures the experience of a first-time merchant perfectly.↩

- When fighting fraud, the accuracy vs precision trade-offs depends on your margin. This is well-covered by Stripe Radar's primer.↩

- The card fees are simplified. In reality they are much more opaque and vary card by card. But the economics net out to something similar to a 1% difference in cost between certain debit cards and some premium cards, which is enough to illustrate the problem. For a quick explanation of these fees, see Interchange in 1,000 words↩

- Cash users suffer more than debit card users in that they are paying this invisible interchange tax and they are not even getting the basic benefit of a bank account and having to carry the cash around.↩

- If you know of any projects that are building services related to what this post covered, please send them to me at sbensu@gmail.com↩